Introduction

As the industry evolves, the demand for efficiency has led compliance teams to reevaluate their onboarding models. However, as the complexities of money laundering regulations increase, so do the challenges faced by compliance professionals. Unlocking efficiencies without compromising the effectiveness of AML measures has become a primary goal for these teams.

In this article, we explore the four most common KYC onboarding models and analyse the advantages and challenges of each. We will also share some observations about which model might suit which type of business.

In our experience, there are four typical models for taking on new clients which we describe below.

- Decentralised KYC

- Centralised KYC

- Hybrid KYC

- Outsourced KYC

Useful definitions

- ‘Relationship Manager’ is used to describe the person bringing the new client relationship into the firm. This could be a banker, fee-earner or accountant.

- ‘Onboarding’ is used to describe all the necessary steps to be taken to comply with the necessary AML regulations when entering into a relationship with a new client.

- ‘KYC unit’ is used to describe a function to whom the Relationship Manager delegates some, or all, of the KYC onboarding tasks.

- ‘Screening’ is used in this article to include screening for Politically Exposed Persons (‘PEPs’), Sanctions and Adverse Media/Negative News.

- ‘Know Your Customer’ (‘KYC’) describes the steps to be taken to identify and verify a client and understand their financial profile and the objectives for the relationship.

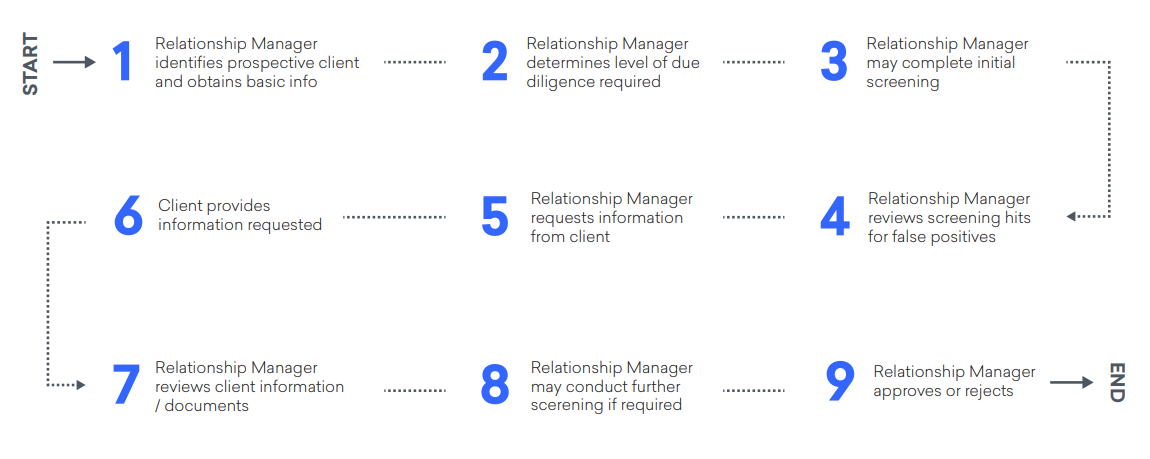

1. Decentralised KYC

In this model, the Relationship Manager (usually a frontline fee-earner in professional services) is responsible for completing all on-boarding tasks. This is ‘decentralised’ KYC/CDD - that is, there is no central unit managing the flow, and every Relationship Manager follows and manages their own cases.

Relationship Managers are responsible for each stage of the process, including determining the level of due diligence required, identification and verification requirements, screening, reviewing documentation received from the client, and ultimately approving the new relationship. In some instances, there may be a ‘four-eyes’ check on the formal approval and/or the KYC documentation, for example case review by a senior manager.

Pros

- Typically, it will be the Relationship Manager, who is best placed to understand the client, including, for example, the ownership of an entity, or the risks in the transaction.

- The Relationship Manager will also be best placed to identify potential red flags regarding the prospective client, such as reluctance to provide information.

Cons

- Onboarding can be an onerous and time-consuming process, taking up either chargeable time or time that would otherwise be spent generating new business.

- Relationship Managers will require regular training, together with access to policies, procedures and tools (such as workflows and screening tools) to complete the necessary KYC checks.

- Relationship Managers may not be consistent in their application of the procedures.

This model ensures that those who might bring money laundering risks into the business are responsible for identifying and mitigating those risks. If volumes of new clients are relatively low, this model may be the most suitable. It is important to note that there should be independent monitoring and evaluation to ensure that the controls applied by the Relationship Managers are being applied consistently and effectively.

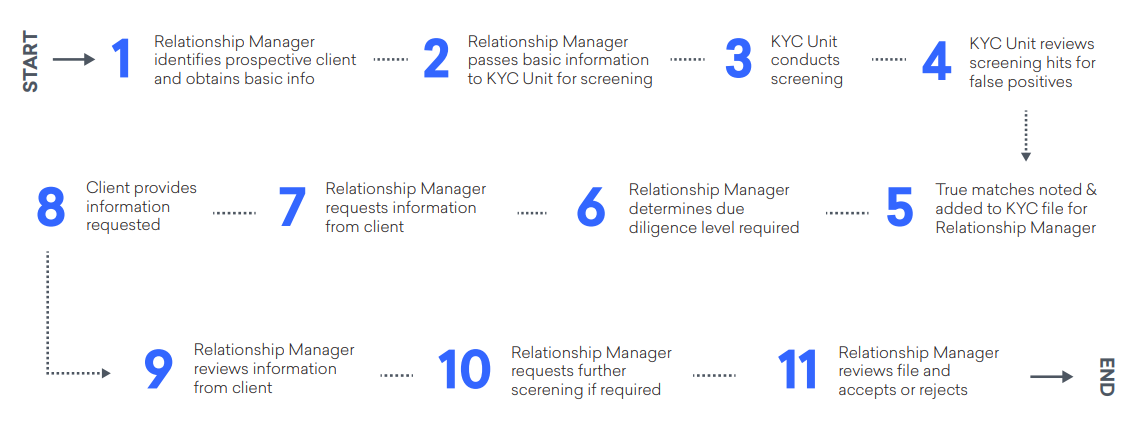

2. Centralised KYC Unit

A dedicated KYC Unit assumes the responsibility for identifying documentation required, obtaining and reviewing the documents from the client, conducting screening and reviewing any screening ‘hits’ to identify and eliminate ‘false positives’. Normally in this scenario, the Relationship Manager will retain responsibility for reviewing the completed KYC files and any issues identified, and as well as providing final approval of the client relationship.

In essence, the Relationship Manager is effectively delegating documentation collection and review, rather than the final decision. In some instances the KYC Unit will have the final approval, but this is very unusual.

Pros

- Relationship Managers can concentrate on fee-earning and/or business development rather than expend time on non-value-adding ‘administrative’ duties.

- Economies of scale and creation of a ‘centre of excellence’ where KYC specialists run the process.

- KYC Unit can filter out false positive matches from screening, ensuring that the Relationship

- Manager only needs to review actual or potential matches.

- Consistency of internal AML processes

Cons

- Relationship Managers may prefer to manage the process and communications with the prospective client.

- KYC Unit will not have the personal knowledge of the client and/or transaction(s).

- Cost of specialist KYC Unit (but this may be offset by efficiency savings for Relationship Managers).

- Identifying experienced resources to staff can be challenging.

This model is typically suited to for Relationship Managers with high volumes of new clients. Where Relationship Managers manage large numbers of clients, it often makes sense to delegate some of the more routine parts of the onboarding process to a specialist support unit. This will ensure that the Relationship Managers have ready access to all the information required to enable them to make decisions on the prospective client.

3. Hybrid model

The Relationship Manager deals with all of the KYC requirements, supported by the KYC Unit. This support may be limited to simply screening the prospective client. Typically, the KYC Unit will also provide some additional support, for example obtaining KYC documents and/or information from publicly available sources. The Relationship Manager approves the relationship based on information gathered by the Relationship Manager and screening completed by the KYC Unit.

Pros

- The Relationship Manager retains control of communications with the client.

- Lower value activities (such as reviewing screening hits to identify false positives) will not take up Relationship Manager time

Cons

- Cost of specialist KYC Unit (but this may be offset by efficiency savings for RMs).

- It would be advisable for the KYC unit to be subject to regular monitoring to ensure it is handling matches effectively.

The Hybrid model is typically suited to businesses with moderate levels of new clients. The approach separates out some of the more time-consuming and administrative tasks allowing the Relationship Manager to focus on the higher value activity. We have seen situations where the Hybrid KYC Unit evolves into the full KYC Unit.

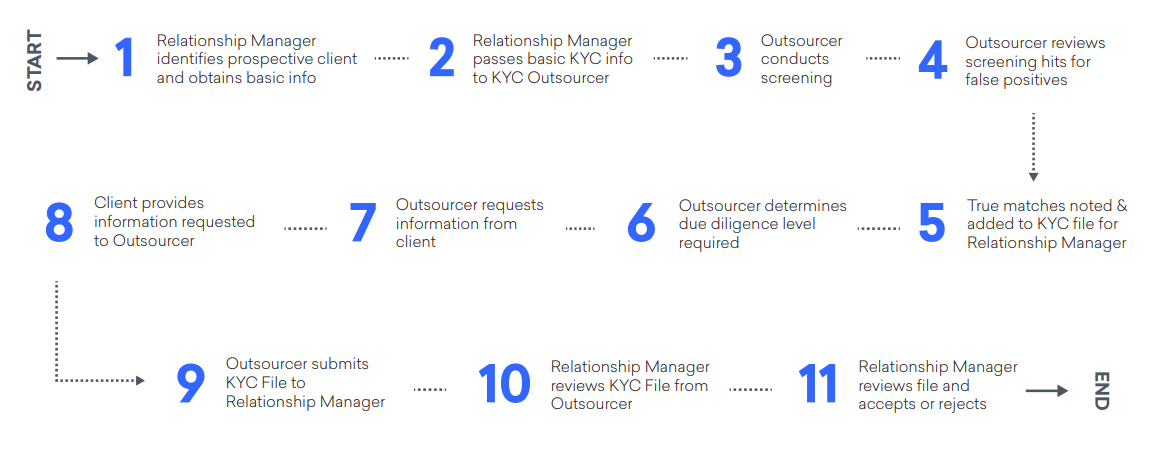

4. Outsourced model

Where an organisation operates with an outsourced model, all KYC activity is outsourced to a specialist third party with the tools, technology and expertise to manage the onboarding process, in accordance with the firm’s policies and procedures.

Under this model, the third party acts as the agent of the organisation. The best outsourcing providers align with the organisation’s own internal process, which results in a smooth and streamlined process for the Relationship Managers and the clients.

It’s important to note that even under an outsourced model, the risk and liability itself is not outsourced. It remains up to the organisation (typically their compliance team or Relationship Manager) to decide the ultimate outcome, having reviewed the information and documentation that the third party has provided.

This model is often most suited for small organisations where the compliance function is being handled by someone else who has another ‘day job’ - e.g. a partner who is also the MLRO, or an administrative assistant who has been managing the AML checks as part of his or her onboarding tasks.

Pros

- Time is freed up by both Relationship Managers and other internal staff.

- Speed – specialists can typically complete the KYC onboarding much more efficiently than the other models.

- Flexibility – outsourcers can typically flex resources to deal with peaks and troughs of onboarding activity.

- Experts – can handle any tricky fringe cases that would be outside the knowledge of non-specialists.

Cons

- Cost - managed services can appear to be more expensive than alternatives, although can sometimes still be more affordable than hiring additional KYC analysts.

- Managed services may not deviate from their procedures and align with the business.

- Concern that Relationship Managers do not ‘own’ the relationship.

Conclusion

Each of the most common models have their respective advantages and challenges. As compliance officers, it is crucial to understand that the choice of the onboarding model should be tailored to the specific needs and volume of clients in the business. Decentralised KYC allows Relationship Managers to take direct responsibility for risk identification and mitigation, whereas centralised or outsourced models offer efficiency benefits for firms dealing with high client volumes. Meanwhile, for those with moderate client levels, a hybrid Model might strike the right balance.

Irrespective of the model chosen, compliance officers should emphasise the importance of independent monitoring evaluation to ensure consistent and effective application of their firms’ risk assessment. By making informed decisions about the appropriate onboarding model and implementing robust processes, compliance teams can safeguard their businesses against money laundering risks and maintain regulatory compliance with confidence.

This article was written in partnership with New Link Consulting.

About New Link Consulting

New Link Consulting provides best-in-class consulting services to clients in the Financial Services industry, including buy-side, sell–side and market intermediaries. They uniquely combine deep industry knowledge with change management skills to deliver their services, including Business Consulting, Industry Solutions and Managed Services. Innovation is at the heart of what they do – from core service delivery through to their approach to developing industry-wide solutions.

About First AML

First AML comes from the perspective of both a technology provider, but also as compliance professionals. Prior to releasing First AML’s all-in-one AML workflow platform, we processed over 2,000,000 AML cases ourselves. Understanding the acute problem that faces firms these days as they try to scale their own AML, is in our DNA.

That's why First AML now powers thousands of compliance experts around the globe to reduce the time and cost burden of complex and international entity KYC. Source stands out as a leading solution for organisations with complex or international onboarding needs. It provides streamlined collaboration and ensures uniformity in all AML practices.

Keen to find out more? Book a demo today!